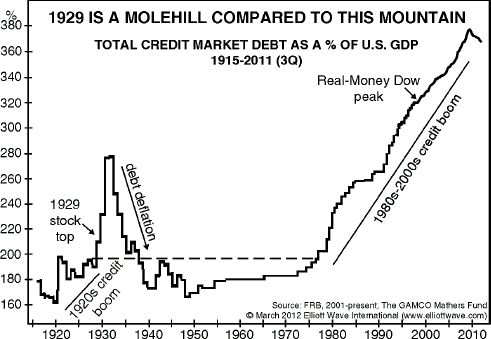

David Stockman: We are in the last innings of a very bad ball game. We are coping with the crash of a 30-year–long debt super-cycle and the aftermath of an unsustainable bubble.

Quantitative easing is making it worse by facilitating more public-sector borrowing and preventing debt liquidation in the private sector—both erroneous steps in my view. The federal government is not getting its financial house in order. We are on the edge of a crisis in the bond markets. It has already happened in Europe and will be coming to our neighborhood soon.

TGR: What should the role of the Federal Reserve be?

DS: To get out of the way and not act like it is the central monetary planner of a $15 trillion economy. It cannot and should not be done.

The Fed is destroying the capital market by pegging and manipulating the price of money and debt capital. Interest rates signal nothing anymore because they are zero. The yield curve signals nothing anymore because it is totally manipulated by the Fed. The very idea of “Operation Twist” is an abomination.

Capital markets are at the heart of capitalism and they are not working. Savers are being crushed when we desperately need savings. The federal government is borrowing when it is broke. Wall Street is arbitraging the Fed’s monetary policy by borrowing overnight money at 10 basis points and investing it in 10-year treasuries at a yield of 200 basis points, capturing the profit and laughing all the way to the bank. The Fed has become a captive of the traders and robots on Wall Street.

TGR: If we are in the final innings of a debt super-cycle, what is the catalyst that will end the game?

DS: I think the likely catalyst is a breakdown of the U.S. government bond market. It is the heart of the fixed income market and, therefore, the world’s financial market.

Because of Fed management and interest-rate pegging, the market is artificially medicated. All of the rates and spreads are unreal. The yield curve is not market driven. Supply and demand for savings and investment, future inflation risk discounts by investors—none of these free market forces matter. The price of money is dictated by the Fed, and Wall Street merely attempts to front-run its next move.

As long as the hedge fund traders and fast-money boys believe the Fed can keep everything pegged, we may limp along. The minute they lose confidence, they will unwind their trades.

On the margin, nobody owns the Treasury bond; you rent it. Trillions of treasury paper is funded on repo: You buy $100 million (M) in Treasuries and immediately put them up as collateral for overnight borrowings of $98M. Traders can capture the spread as long as the price of the bond is stable or rising, as it has been for the last year or two. If the bond drops 2%, the spread has been wiped out.

If that happens, the massive repo structures—that is, debt owned by still more debt—will start to unwind and create a panic in the Treasury market. People will realize the emperor is naked.

TGR: Is that what happened in 2008?

DS: In 2008 it was the repo market for mortgage-back securities, credit default obligations and such. In 2008 we had a dry run of what happens when a class of assets owned on overnight money goes into a tailspin. There is a thunderous collapse.

Since then, the repo trade has remained in the Treasury and other high-grade markets because subprime and low-quality mortgage-backed securities are dead.

TGR: Walk us through a hypothetical. What happens when the fast-money traders lose confidence in the Fed’s ability to keep the spread?

DS: They are forced to start selling in order to liquidate their carry trades because repo lenders get nervous and want their cash back. However, when the crisis comes, there will be insufficient private bids—the market will gap down hard unless the central banks buy on an emergency basis: the Fed, the European Central Bank (ECB), the people’s printing press of China and all the rest of them.

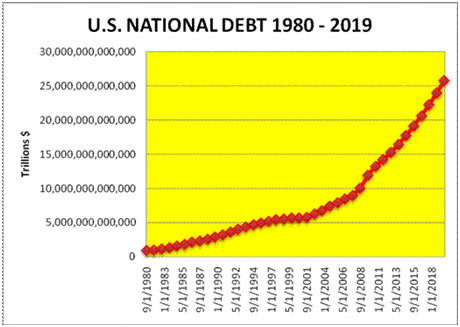

The question is: Will the central banks be able to do that now, given that they have already expanded their balance sheets? The Fed balance sheet was $900 billion (B) when Lehman crashed in September 2008. It took 93 years to build it to that level from when the Fed opened for business in November 1914. Bernanke then added another $900B in seven weeks and then he took it to $2.4 trillion in an orgy of money printing during the initial 13 weeks after Lehman. Today it is nearly $3 trillion. Can it triple again? I do not think so. Worldwide it’s the same story: the top eight central banks had $5 trillion of footings shortly before the crisis; they have $15 trillion today. Overwhelmingly, this fantastic expansion of central bank footings has been used to buy or discount sovereign debt. This was the mother of all monetizations.

TGR: Following that path, what happens if there are no buyers? Do the governments go into default?

DS: The U.S. Treasury needs to be in the market for $20B in new issuances every week. When the day comes when there are all offers and no bids, the music will stop. Instead of being able to easily pawn off more borrowing on the markets—say 90 basis points for a 5-year note as at present—they may have to pay hundreds of basis points more. All of a sudden the politicians will run around with their hair on fire, asking, what happened to all the free money?

TGR: What do the politicians have to do next?

DS: They are going to have to eat 30 years worth of lies and by the time they are done eating, there will be a lot of mayhem.

TGR: Will the mayhem stretch into the private sector?

DS: It will be everywhere. Once the bond market starts unraveling, all the other risk assets will start selling off like mad, too.

TGR: Does every sector collapse?

DS: If the bond market goes into a dislocation, it will spread like a contagion to all of the other asset markets. There will be a massive selloff.

I think everything in the world is overvalued—stocks, bonds, commodities, currencies. Too much money printing and debt expansion drove the prices of all asset classes to artificial, non-economic levels. The danger to the world is not classic inflation or deflation of goods and services; it’s a drastic downward re-pricing of inflated financial assets.

TGR: Is there any way to unravel this without this massive dislocation?

DS: I do not think so. When you are so far out on the end of a limb, how do you walk it back?

The Fed is now at the end of a $3 trillion limb. It has been taken hostage by the markets the Federal Open Market Committee was trying to placate. People in the trading desks and hedge funds have been trained to front run the Fed. If they think the Fed’s next buy will be in the belly of the curve, they buy the belly of the curve. But how does the Fed ever unwind its current lunatic balance sheet? If the smart traders conclude the Fed’s next move will be to sell mortgage-backed securities, they will sell like mad in advance; soon there would be mayhem as all the boys and girls on Wall Street piled on. So the Fed is frozen; it is petrified by fear that if it begins contracting its balance sheet it will unleash the demons.

TGR: Was there some type of tipping that allowed certain banks to front run the Fed?

DS: There are two kinds of front-running. First is market-based front-running. You try to figure out what the Fed is doing by reading its smoke signals and looking at how it slices and dices its meeting statements. People invest or speculate against the Fed’s next incremental move.

Second, there is illicit front-running, where you have a friend who works for the Federal Reserve Board who tells you what happened in its meetings. This is obviously illegal.

But frankly, there is also just plain crony capitalism that is not that different in character and it’s what Wall Street does every day. Bill Dudley, who runs the New York Fed, was formerly chief economist for Goldman Sachs and he pretends to solicit an opinion about financial conditions from the current Goldman economist, who then pretends to opine as to what the economy and Fed might do next for the benefit of Goldman’s traders, and possibly its clients. So then it links in the ECB, Bank of Canada, etc. Is there any monetary post in the world not run by Goldman Sachs?

The point is, this is not the free market at work. This is central bank money printers and their Wall Street cronies perverting what used to be a capitalist market.

TGR: Does this unwinding of the Fed and the bond markets put the banking system back in peril, like in 2008?

DS: Not necessarily. That is one of the great myths that I address in my book. The banking system, especially the mainstream banking system, was not in peril at all. The toxic securitized mortgage assets were not in the Main Street banks and savings and loans; these institutions owned mostly prime quality whole loans and could have bled down the modest bad debt they did have over time from enhanced loan loss reserves. So the run on money was not at the retail teller window; it was in the canyons of Wall Street. The run was on wholesale money—that is, on repo and on unsecured commercial paper that had been issued in the hundreds of billions by financial institutions loaded down with securitized toxic garbage, including a lot of in-process inventory, on the asset side of their balance sheets.

The run was on investment banks that were really hedge funds in financial drag. The Goldmans and Morgan Stanleys did not really need trillion-dollar balance sheets to do mergers and acquisitions. Mergers and acquisitions do not require capital; they require a good Rolodex. They also did not need all that capital for the other part of investment banking—the underwriting business. Regulated stocks and bonds get underwritten through rigged cartels—they almost never under-price and really don’t need much capital. Their trillion dollar balance sheets, therefore, were just massive trading operations—whether they called it customer accommodation or proprietary is a distinction without a difference—which were funded on 30 to 1 leverage. Much of the debt was unstable hot money from the wholesale and repo market and that was the rub—the source of the panic.

Bernanke thought this was a retail run à la the 1930s. It was not; it was a wholesale money run in the canyons of Wall Street and it should have been allowed to burn out.

TGR: Let’s get back to our ballgame. What is to keep the U.S. population from saying, please Fed save us again?

DS: This time, I think the people will blame the Fed for lying. When the next crisis comes, I can see torches and pitch forks moving in the direction of the Eccles building where the Fed has its offices.

TGR: Let’s talk about timing. On Dec. 31, the tax cuts expire, defense cuts go into place and we hit the debt ceiling.

DS: That will be a clarifying moment; never before have three such powerful vectors come together at the same time— fiscal triple witching.

First, the debt ceiling will expire around election time, so the government will face another shutdown and it will be politically brutal to assemble a majority in a lame duck session to raise it by the trillions that will be needed. Second, the whole set of tax cuts and credits that have been enacted over the last 10 years total up to $400–500B annually will expire on Dec. 31, so they will hit the economy like a ton of bricks if not extended. Third, you have the sequester on defense spending that was put in last summer as a fallback, which cannot be changed without a majority vote in Congress.

It is a push-pull situation: If you defer the sequester, you need more debt ceiling. If you extend the tax expirations, you need a debt ceiling increase of $100B a month.

TGR: What will Congress do?

DS: Congress will extend the whole thing for 60 or 90 days to give the new president, if he hasn’t demanded a recount yet, an opportunity to come up with a plan.

To get the votes to extend the debt ceiling, the Democrats will insist on keeping the income and payroll tax cuts for the 99% and the Republicans will want to keep the capital gains rate at 15% so the Wall Street speculators will not be inconvenienced. It is utter madness.

TGR: It is like chasing your tail. How does it stop?

DS: I do not know how a functioning democracy in the ordinary course can deal with this. Maybe someone from Goldman Sachs can come and put in a fix, just like in Greece and Italy. The situation is really that pathetic.

TGR: Greece has come up with some creative ways to bring down its sovereign debt without actually defaulting.

DS: The Greek debt restructuring was a farce. More than $100B was held by the European bailout fund, the ECB or the International Monetary Fund. They got 100 cents on the dollar simply by issuing more debt to Greece. For private debt, I believe the net write-down was $30B after all the gimmicks, including the front-end payment. The rest was simply refinanced. The Greeks are still debt slaves, and will be until they tell Brussels to take a hike.

TGR: Going back to the triple-witching hour at year-end, if the debt ceiling is raised again, when do we start to see government layoffs and limitations on services?

DS: Defense purchases and non-defense purchases will be hit with brutal force by the sequester. As we go into 2013, there will be a shocking hit to the reported GDP numbers as discretionary government spending shrinks. People keep forgetting that most government spending is transfer payments, but it is only purchases of labor and goods that go directly into the GDP calculations, and it is these accounts that will get smacked by the sequester of discretionary defense and non-defense budgets.

TGR: I would think to unemployment numbers as well.

DS: They will go up.

Just take one example. According to the Bureau of Labor Statistics monthly report, there are 650,000 or so jobs in the U.S. Postal Service alone. That is 650,000 people who pretend to work at jobs that have more or less been made obsolete and redundant by the Internet and who are paid through borrowings from Uncle Sam because the post office is broke. Yet, the courageous ladies and gentlemen on Capitol Hill cannot even bring themselves to vote to discontinue Saturday mail delivery; they voted to study it! That is a measure of the loss of capacity to rationally cognate about our fiscal circumstance.

TGR: In the midst of this volatility, how can normal people preserve, much less expand their wealth?

DS: The only thing you can do is to stay out of harm’s way and try to preserve what you can in cash. All of the markets are rigged or impaired. A 4% yield on blue chip stocks is not worth it, because when the thing falls apart, your 4% will be gone in an hour.

TGR: But if the government keeps printing money, cash will not be worth as much, either, right?

DS: No, I do not think we will have hyperinflation. I think the financial system will break down before it can even get started. Then the economy will go into paralysis until we find the courage, focus and resolution to do something about it. Instead of hyperinflation or deflation there will be a major financial dislocation, which means painful re-pricing of financial assets.

How painful will the re-pricing be? I think the public already knows that it will be really terrible. A poll I saw the other day indicated that 25% of people on the verge of retirement think they are in such bad financial shape that they will have to work until age 80. Now, the average life expectancy is 78. People’s financial circumstances are so bad that they think they will be working two years after they are dead!

TGR: Finally, what is your investment model?

DS: My investing model is ABCD: Anything Bernanke Cannot Destroy: flashlight batteries, canned beans, bottled water, gold, a cabin in the mountains.

TGR:Thank you very much.

David Stockman is a former U.S. politician and businessman, serving as a Republican U.S. Representative from the state of Michigan 1977–1981 and as the director of the Office of Management and Budget under President Ronald Reagan 1981–1985. He is the author of The Triumph of Politics: Why Reagan’s Revolution Failed and the soon-to-be released The Great Deformation: How Crony Capitalism Corrupts Free Markets and Democracy.

Stockman was the keynote speaker at last weekend’s Casey Research Recovery Reality Check Summit. This event featured legendary contrarian investor Doug Casey, high-end natural resource broker Rick Rule, New York Times bestselling author John Mauldin and 28 other financial luminaries. Over the three-day summit, they provided investors with asset-protection action plans and actionable investment advice.

A “paralyzed” Federal Reserve Bank, in its “final days,” held hostage by Wall Street “robots” trading in markets that are “artificially medicated” are just a few of the bleak observations shared by David Stockman, former Republican U.S. Congressman and director of the Office of Management and Budget. He is also a founding partner of Heartland Industrial Partners and the author of The Triumph of Politics: Why Reagan’s Revolution Failed and the soon-to-be released The Great Deformation: How Crony Capitalism Corrupts Free Markets and Democracy.

A “paralyzed” Federal Reserve Bank, in its “final days,” held hostage by Wall Street “robots” trading in markets that are “artificially medicated” are just a few of the bleak observations shared by David Stockman, former Republican U.S. Congressman and director of the Office of Management and Budget. He is also a founding partner of Heartland Industrial Partners and the author of The Triumph of Politics: Why Reagan’s Revolution Failed and the soon-to-be released The Great Deformation: How Crony Capitalism Corrupts Free Markets and Democracy.

(1).jpg)