The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

The Daily Show

Get More: Daily Show Full Episodes,The Daily Show on Facebook

One of the cool things about the Bible is that it contains some very interesting passages that no one seems to read.

Understand, please, that I’m neither promoting a literal interpretation of the Bible nor giving you a sermon. I’m just pointing out a fascinating fact that most everyone seems to have missed, religious folks included.

In this case, I’m referring to a passage that comes at the very end of the book, where a list is given, itemizing the kinds of people who will be condemned to “the second death.”

Who would you expect to stand at the top of the list? Murders? Idolators? Maybe adulterers?

Nope, none of those. The first people heading off to destruction are “the fearful.”

But the fearful, and unbelieving, and the abominable, and murderers, and whoremongers, and sorcerers, and idolaters, and all liars, shall have their part in the lake which burneth with fire and brimstone: which is the second death.

Not what you expected?

You can look it up if you like. That’s from Revelation 21:8 (King James Version). And I even checked the original Greek: fearful is the right translation.

I’m not going to get into theological engineering here, but yes, this would mean that the promoters of fear are sending people to hell.

And, considering that we live in a fear-based culture, that’s an interesting thought indeed.

Now, if you want to be truly bold, think about this: Who is it that currently promotes fear?

We know the answer, of course. The people who live on fear are the majesties of the age: politicians being chief among them but followed by the entire ‘law enforcement‘ complex, military and intelligence organizations, television news-readers, religious bosses, newspaper operators, and, increasingly, anyone who wants something and has access to the public stage.

If the Bible is correct, people who profit from fear are profiting from the destruction (nay, the damnation!) of their fellow men and women.

The conclusion that fear is the enemy of mankind doesn’t require religion, of course. We can reach the same conclusion just by recognizing that fear (and especially the chemicals associated with fear) damage our health.

Literally, people who make you fear are making you sick. (We covered this in issue #38 of Free-Man’s Perspective)

Beyond that, it is clear that fear is the number one tool of manipulators. If you want to get large numbers of men and women to do your will, scare them. Every tyrant in history has known this and used this technique.

First of all, start paying attention to your feelings and notice when things make you afraid. Stop your thinking and pay attention to the whole fear process. If you do, you can deal with most of these attacks quickly, rather than leaving an indistinct fear to roll around the back of your mind all day.

Second, start analyzing the words that convey fear to you. Are they really true? Is the response the fear merchants deliver to you really the only course of action? The hard part of doing this is that the words come too fast; by the time you’re ready to analyze one statement, another one is halfway complete. Analyzing them in writing is far easier, or getting a live speaker to slow down and go one phrase at a time.

Third, start discounting the people who consistently throw fear at you. If that’s all they have, they’re not worth paying attention to. Turn off the TV; excuse yourself from the conversation; walk away. You don’t have to take it.

Finally, start pointing out these things to other people. They may be defensive at first, but isn’t that worth facing, to clear the minds of your friends and family? Why should they suffer under the lash of fear all their lives?

Paul Rosenberg

[Editor’s Note: Paul Rosenberg is the outside-the-Matrix author of FreemansPerspective.com, a site dedicated to economic freedom, personal independence and privacy. He is also the author of The Great Calendar, a report that breaks down our complex world into an easy-to-understand model. Click here to get your free copy.]

I had a conversation the other day with the best and most knowledgeable computer guy I know. After discussing privacy threats, he made this statement:

Everybody buying a Windows computer today is a traitor to humanity.

Now, this is a very technically oriented guy, and he quickly agreed with me that most people don’t have a clue about such things. Still, the primary point stands: Whenever any of us buys a Microsoft product, we are supporting the tools of our own slavery.

Here’s the problem:

Because people keep buying Windows, computer manufacturers are forced to buy and provide “Licensed for Windows” products. And those products include a lot of bad things. As I’ve pointed out before, Microsoft cooperates massively with the NSA to provide them with records of your thoughts and actions. But the problem my friend referred to was something else… something called TPM,

Trusted Platform Module.

It’s a little chip in your computer that is, in my friend’s words, “way evil.”

Microsoft’s goal (with Apple following in their footsteps, by the way) is to kill the general purpose computer. Combining this Trusted Platform Module with Windows provides something that Microsoft and their government pals have been after for a number of years: something called Digital Hygiene.

If that sounds slightly Nazi-ish to you, I’m glad, because it is.

Digital Hygiene means that unless Microsoft approves of all the software on your computer – or any number of other factors, to be determined in the future – your Internet access will be instantly cut-off.

Here’s what Microsoft’s Corporate Vice President of Trustworthy Computing was quoted as saying (by multiple sources, at a conference in Berlin) in 2010:

Infected computers should be quarantined from the Internet, and PCs should have to prove themselves clean with a digital health certificate in order to access the Internet.

Now they are doing it, and my friend is right to raise an alarm.

More and more computers cannot run anything except a “signed” operating system – signed by Microsoft or the hardware manufacturer. In other words, if they haven’t given the A-OK that what you’re using is as it should be, you get cut off. Moreover, the “we certify it or what you bought won’t work” extends to every program you run.

This is already inside any computer that is sold as “Ready for Windows 8.” When you install Windows 8, these capabilities are automatically activated.

Once that’s done, you will need major computer skills to wipe it off your machine and install something better.

What this all means is that, in the not too distant future – if you use a Windows machine – you might be limited to a small selection of pre-approved, pre-sanitized, privacy-questionable programs.

And I can almost guarantee all the tools we use now to protect ourselves from the reach of digital snoops will be blocked too, leaving us naked and vulnerable.

Buy a Linux machine. Not only will it protect you against the above, but it’ll be cheaper, and doesn’t have all the problems that Windows does (e.g., the blue screen of death).

Here’s how to get started:

Most likely, unless you’re technically minded, you’ll need to enlist the help of your local independent computer retailer. Do so – they will be a great resource as you shift to a non-Microsoft world.

Remember, Microsoft is a traitor to their customers, relying upon their ignorance to keep the game going.

Don’t be their zombies!

[Editor’s Note: Paul Rosenberg is the outside-the-Matrix author of FreemansPerspective.com, a site dedicated to economic freedom, personal independence and privacy. He is also the author of The Great Calendar, a report that breaks down our complex world into an easy-to-understand model. Click here to get your free copy.]

Well, at least the poobahs cleared a path to the annual orgy of Christmas, which, along with the S & P 500, have become proxies for the American economy. Lately, the Christmas season starts directly after Halloween, so, the whole fourth quarter of the year becomes a circus of ceremonial distractions. In the background, though, the nation grinds toward anguish, measured in soiled Justin Bieber dolls deposited in the landfills.

Historians who look back on these strange years of suspended consequence will marvel at how this empire of grift kept its wheels turning after its engine died. Being on the downhill slope is often enough to keep anything going. One might think the young people of this land would be seething at the eclipse of their futures, but it seems they have been successfully lobotomized with cell phones — when the endorphin hits lag between text messages, they can watch sitcoms, or porn.

You can be sure there will be a snapback from all this drift and anomie, and when it comes, the snap will be savage. Like the US economy, the Republican Party is dead but hasn’t gotten the news. It killed itself just as the Whigs did in the years before the Civil War, by splitting up into factions — one faction of “know-nothings” preoccupied with scape-goats opposed to a faction of sclerotic parasitical fat-cats too timid and greedy to engage in the emergencies of the day.

The Tea Party faction should change its name to the Cracker Party because it represents the interests of white southerners who are too dumb to know what these emergencies amount to. They are really more comfortable with the supernatural, hence their fondness for religions based on snake-handling, visitations of the dead, and motor sports. Personally, I believe they will eventually contrive to form their own break-away Cracker Republic and attempt to re-enact the Civil War. They will fail, and starve, and find themselves back in an even worse long-term depression than Dixieland experienced from 1860 to 1960, in a de-suburbanized wasteland of bare subsistence farming. Their highest art will be soup-making.

The non-Tea Party Republicans will just shrivel and vanish out of sheer irrelevance. This leaves the Democrats to become the focus of intense ire as they attempt to ‘splain why the nation’s affairs went to shit on their watch. A lot of them will end up being executed and plundered by the new kid on the block, the Savior Party, led by some charismatic character willing to ignore procedural protocols to clear away the debris left by his-or-her predecessors. Alas, the juice will not be there to permit the Savior to really control a territory as large as the continental USA. By juice, I mean money and oil. Thus, the nation enters its new dark age.

Who knows when that will get underway in earnest, though I think the folks who say 2014 are onto something. If you believe in cycles, which I tend to, then it rhymes nicely with 1814 and 1914, two watersheds when one epoch ended and another truly began. 2014 would logically be the year that China tells America to go piss up a rope. The message would be sent on the back of the envelope containing $2.7 trillion in official American debt paper. As Ole Blue Eyes used to say, this could be the start of something big.

Sentient observers of the current scene are clearly frustrated by the remarkable homeostasis that seems to rule the scene, these horse-latitudes of history where the air is still and nothing moves and the mind is exhausted by watchful waiting. Things will get lively, soon enough, so enjoy the holiday quarter of the year which is so soon upon us. Gorge on candy corn. When you recover from that, roast a turkey. Then make a nice figgy pudding. Then pop some bubbly and salute your loved ones. Then gird your loins for the new age of consequence.

“For as long as I can remember, veteran businessmen and investors – I among them – have been warning about the dangers of irrational stock speculation and hammering away at the theme that stock certificates are deeds of ownership and not betting slips… The professional investor has no choice but to sit by quietly while the mob has its day, until the enthusiasm or panic of the speculators and non-professionals has been spent. He is not impatient, nor is he even in a very great hurry, for he is an investor, not a gambler or a speculator. The seeds of any bust are inherent in any boom that outstrips the pace of whatever solid factors gave it its impetus in the first place. There are no safeguards that can protect the emotional investor from himself.” – J. Paul Getty

Another fact filled truthful warning from John Hussman. We might be in the midst of a blow-off top that will take the markets to marginal new highs, but the hangover will be epic and ten years from now, the stock market will be no higher than it is today. If you are too lazy to read the whole article, these two paragraphs will provide the insight you need to take away from this post:

On a diverse set of reliable fundamentals, we now estimate a 10-year nominal total return for the S&P 500 of just 2.6% annually. Put another way, stocks are likely to achieve zero risk premium over 10-year Treasuries in the coming decade, despite having about five times the duration, volatility and drawdown risks. The entirety of that total return can be expected to arrive in the form of dividends, leaving the S&P 500 below its current level a decade from now. This would be a less depressing conclusion if I didn’t correctly say the same thing in 2000, and if even simple versions these valuation methods didn’t have a nearly 90% correlation with subsequent 10-year returns (see Investment, Speculation, Valuation, and Tinker Bell).

The failure of investors to learn from experience isn’t just an inconvenience – the constant misallocation of capital resulting from these speculative episodes is gradually destroying our nation’s economic potential for long-term growth and job creation. We measure our standard of living by the amount of output that an individual is able to command for a given amount of work. We measure our productivity by the amount that an individual is able to produce for a given amount of work. Over time, these two must go hand in hand. Policies that misallocate savings away from productive investment and toward unproductive speculation are the same policies that do long-term violence to our nation’s standard of living. Although the members of the Federal Reserve undoubtedly mean well, their actions are at the center of the assault.

Bernanke has solved nothing. The economy has been terminally damaged by his actions. Accounting fraud does not change the fact that Wall Street banks, Fannie Mae, Freddie Mac, the Federal Reserve, and our local, state and federal governments are effectively bankrupt and insolvent. Throwing freshly printed pieces of paper at a debt problem is as mind boggling as it is insane. Enjoy the show while it lasts.

John P. Hussman, Ph.D.

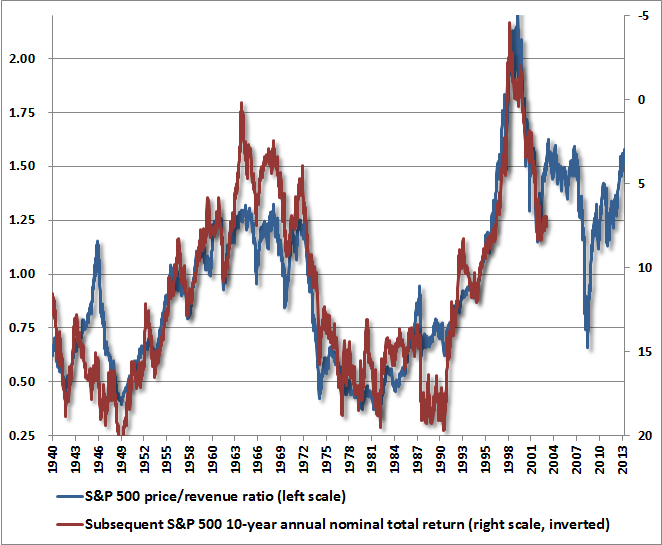

As investors, we should be aware that the current Shiller P/E of 24.8 (S&P 500 divided by the 10-year average of inflation adjusted earnings) is now above every historical instance prior to the bubble period since the late-1990’s, save for the final weeks approaching the 1929 peak. We should also be aware that overvaluation alone in the late-1990’s did not stop the market from reaching even higher levels as new-era speculation culminated in the 2000 bubble peak.

It’s fine, and quite accurate to say that valuations are not as frenzied as they were at the 2000 extreme (a comparison that fell from the lips of Robert Shiller himself last week), provided that one also recognizes that the hypervaluation in 2000 has been followed by a period that included two separate market losses in excess of 50%, and a nominal total return from 2000 until today averaging just 3.2% annually. Even that weak 13-year return has been achieved only thanks to distortions that have again driven present valuations to temporary and historically untenable extremes.

Put simply, the past 13 years have chronicled the journey of valuations – from hypervaluation to levels that still exceed every pre-bubble precedent other than a few weeks in 1929. If by 2023, stock valuations complete this journey not by moving to undervaluation, but simply by touching pre-bubble norms, we estimate that the S&P 500 will have achieved a nominal total return of only about 2.6% annually between now and then.

What usually distinguishes an overvalued market that continues to advance from an overvalued market that drops like a rock is the quality of market internals and related measures that capture the preference of investors to seek risk. On that front, our views on near-term return/risk prospects are very mixed at present. On one hand, our primary measures of market internals remain unfavorable but approaching borderline, while price action appears overbought on nearly every measure. On the other hand, bullish sentiment has eased back modestly, and investors continue to celebrate the likelihood that the Fed will defer any tapering decision this month. More on short-term considerations below.

Examining various historically useful fundamentals, the S&P 500 price/revenue ratio of 1.6 is now twice its pre-bubble historical norm of about 0.8. For perspective, it’s worth noting that the 1987 peak occurred at a price/revenue ratio of less than 1.0 and neither the 1965 secular valuation peak, nor the 1972 peak (before stocks dropped in half) breached even 1.3. Also, take care to note that the price/revenue multiple is twice the historical median – not twice the level where bear markets have typically ended. No, the price/revenue ratio is closer to three times that level.

Broadening our view to a larger set of historically reliable measures that are actually well-correlated with subsequent market returns, we arrive at identical conclusions. For example, the market value of non-financial stocks to GDP (based on Z.1 flow-of-funds data from the Federal Reserve) presently works out to about 1.24. This is twice the pre-bubble norm, well above the 2007 peak, and already at late-1999 levels.

On a diverse set of reliable fundamentals, we now estimate a 10-year nominal total return for the S&P 500 of just 2.6% annually. Put another way, stocks are likely to achieve zero risk premium over 10-year Treasuries in the coming decade, despite having about five times the duration, volatility and drawdown risks. The entirety of that total return can be expected to arrive in the form of dividends, leaving the S&P 500 below its current level a decade from now. This would be a less depressing conclusion if I didn’t correctly say the same thing in 2000, and if even simple versions these valuation methods didn’t have a nearly 90% correlation with subsequent 10-year returns (see Investment, Speculation, Valuation, and Tinker Bell).

The failure of investors to learn from experience isn’t just an inconvenience – the constant misallocation of capital resulting from these speculative episodes is gradually destroying our nation’s economic potential for long-term growth and job creation. We measure our standard of living by the amount of output that an individual is able to command for a given amount of work. We measure our productivity by the amount that an individual is able to produce for a given amount of work. Over time, these two must go hand in hand. Policies that misallocate savings away from productive investment and toward unproductive speculation are the same policies that do long-term violence to our nation’s standard of living. Although the members of the Federal Reserve undoubtedly mean well, their actions are at the center of the assault.

Did Monetary Policy Cause the Recovery?

We can quite reliably estimate the long-term returns that stocks are likely to deliver over a 7-10 year horizon. Still, valuations often have less direct effect over shorter portions of the market cycle. The present situation is complicated by the fact that while valuations are extreme from a historical standpoint, investors are tied to a narrative that assumes a cause-and-effect link between monetary policy and market direction. The “follow the Fed” narrative certainly did not prevent the market from losing half of its value during the 2000-2002 and 2007-2009 plunges, despite aggressive monetary easing in both instances, but what matters in the short-run is not the truth of that narrative, but the perception that it is true.

Since about 2010, normal economic relationships have taken a back seat to ever larger monetary policy interventions. The correlation between reliable leading measures of economic activity and subsequent job growth and GDP has dropped not just to zero but to negative levels (see When Economic Data is Worse Than Useless). Similarly, extreme overvalued, overbought, overbullish syndromes, which throughout history have been closely followed by severe losses, have instead been followed by further speculative gains. The question is whether this reflects a permanent change in economic dynamics, or a temporary overconfidence about the effectiveness of monetary policy.

To address this question, a proper understanding of the credit crisis is essential. Much of the present faith in monetary policy derives from the belief that it was the central factor in ending the banking crisis during what is often called the Great Recession. On careful analysis, however, the clearest and most immediate event that ended the banking crisis was not monetary policy, but the abandonment of mark-to-market accounting by the Financial Accounting Standards Board on March 16, 2009, in response to Congressional pressure by the House Committee on Financial Services on March 12, 2009. The change to the accounting rule FAS 157 removed the risk of widespread bank insolvency by eliminating the need for banks to make their losses transparent. No mark-to-market losses, no need for added capital, no need for regulatory intervention, recievership, or even bailouts. Misattributing the recovery to monetary policy has contributed to a faith in its effectiveness that cannot even withstand scrutiny of the 2000-2002 and 2007-2009 recessions, and the accompanying market plunges. This faith is already wavering, but the loss of this faith will be one of the most painful aspects of the completion of the present market cycle.

The simple fact is that the belief in direct, reliable links between monetary policy and the economy – and even with the stock market – is contrary to the lessons from a century of history. Among the many things that are demonstrably not true – and can be demonstrated to be untrue even with simple scatterplots – are the notions that inflation and unemployment are negatively related over time (the actual correlation is close to zero and slightly positive), that higher inflation results in lower subsequent unemployment (the actual correlation is positive), that higher monetary growth results in subsequent employment gains (the correlation is almost exactly zero), and a wide range of similarly popular variants. Even “expectations augmented” variants turn out to be useless. Examining historical evidence would be a useful exercise for Econ 101 students, who gain an unrealistic sense of cause and effect as the result of studying diagrams instead of data.

In regard to what is demonstrably true, it can easily be shown that unemployment has a significant inverse relationship with real, after-inflation wage growth. This is the true Phillips Curve, but reflects a simple scarcity relationship between available labor and its real price, but this relationship can’t be manipulated to create jobs (see Will the Real Phillips Curve Please Stand Up). It’s also true that changes in stock prices are mildly correlated with subsequent reductions in the unemployment rate and higher GDP growth. But the effect sizes are strikingly weak. A 1% increase in stock prices correlates with a transitory increase of only 0.03-0.05% in subsequent GDP, and a decline of only about 0.02% in the unemployment rate. So to use the stock market as a policy instrument, the Fed would have to move the stock market about 70% above fair value just to get 2.8% in transitory GDP growth, and a 1.4% decline in the unemployment rate. Guess what? The Fed has done exactly that. The scale of present financial disortion is enormous, and further distortions rely on the permanent belief that there is actually a mechanistic link between monetary policy and stock prices.

We know very well the mechanisms and actual historical relationships between monetary policy and financial markets, and doubt that any amount of quantitative easing will prevent a market slaughter in any environment where investors find short-term liquidity desirable (QE only “works” to the extent that zero-interest liquidity is treated as an undesirable “hot potato”). Still, the novelty of quantitative easing, and the misattributed belief that monetary policy ended the banking crisis, has created financial distortions where perception-is-reality, at least for now. We believe that the modifier “for now” will prove no more durable than it was during the tech bubble or the housing bubble.

On Full-Cycle Discipline

From a short-term perspective, the S&P 500 is pushing its upper Bollinger bands at daily, weekly and monthly resolutions (two standard deviations above the respective 20-period averages), which to say that the recent advance looks stretched. At the same time, though our measures of market internals still show internal divergence, there’s little question that speculation has gathered some momentum. Specifically, monetary “tapering” is likely to be taken off the table for a while, as the result of recent fiscal wrangling, which requires us to allow for the possibility of a speculative blowoff over a handful of weeks. Even if a speculative ramp occurs, it’s not at all clear that speculators will actually be able to get out with much – the first few days off the top are likely to wipe out months of gains in one fell swoop – but again, we have to at least allow for an already reckless situation to become even more reckless over the short run, as the crowd seems to have a bit in its teeth.

In any event, while the potential for further speculation may warrant a bit of insurance (index call options have a useful contingent profile), the most important consideration continues to be the complete cycle, not the next few weeks. As in 2007, we’re back to a situation where fair value is more than 40% below present levels, and I believe that it is essential to maintain a strong defense overall.

If you picture a small child throwing a stone upward and out over the edge of the Grand Canyon, you’ll get a general idea of the market trajectory that we expect over the completion of this cycle.

With regard to catalysts, it’s a market truism that the catalysts become clear only after a bear market is well underway, but my impression is that the primary factor contributing to market losses over the remainder of this cycle will not be some abrupt crisis, but instead a persistent and broadening loss of confidence – not only in the ability of monetary policy to produce economic growth, but in the prospects for economic growth itself. The predictable contraction in corporate profit margins will certainly contribute, but remember that changes in corporate profits typically follow changes in combined government and household savings with a lag of 4-6 quarters, and most of the recent shift in combined savings has only occurred since the third quarter of 2012.

All of this is a mixed situation – one where valuations and long-run evidence are extremely clear, but where perception and sentiment may dominate over the short-run. Our discipline remains to rely on the demonstrated historical evidence, while allowing for some amount of further distortion.

Since 2000, we’ve made only two material changes to our investment discipline – one resulted from stress-testing against Depression-era outcomes that I insisted on in 2009-early 2010 (despite the fact that our existing estimation methods had served admirably to that point), and the other being a smaller hedging adaptation in 2012 (see Notes on An Extraordinary Market Cycle). Our confidence in our discipline follows directly from knowing exactly how our present methods have performed in market cycles across history, including the Depression, including the cycle from 2000-2007, and including the cycle from 2007 to the present. In hindsight, I would undoubtedly prefer to have applied either our present return/risk estimation methods or our pre-2009 methods over the complete course of the most recent cycle, without the unfortunate and awkward transition that the credit crisis provoked. We don’t have that luxury, but to understand the full story of the half-cycle since 2009, and to take either our pre-2009 or present methods to the data (the present ones also covering Depression-era outcomes) is to understand why we adhere to our discipline without blinking. See Aligning Market Exposure with the Expected Return/Risk Profile for the general framework and a very simple illustration of this discipline. As I’ve noted before, history repeatedly teaches a very coherent set of lessons:

Monetary conditions can be a modifier, but have historically not prevented these basic tendencies from dominating over time. Investors who are convinced that this time is different or that following the Fed is some kind of “sure thing” are at liberty to forge their own path and test that hypothesis on their own. We cannot do it for them, nor are we moved by any inclination to do so.

It’s quite popular, at times like these, for people to quote Keynes, saying “the market can remain irrational longer than you can remain solvent,” but insolvency is the problem of debtors and those who speculate on margin, not for those who simply await better opportunities. Keynes actually made that comment because he was wiped out with a leveraged long position in a plunging market.

From my standpoint, the more apt perspective is that of J. Paul Getty (whom I also quoted in 2000, and at the May highs, a few percent from current levels). Getty wrote:

“For as long as I can remember, veteran businessmen and investors – I among them – have been warning about the dangers of irrational stock speculation and hammering away at the theme that stock certificates are deeds of ownership and not betting slips… The professional investor has no choice but to sit by quietly while the mob has its day, until the enthusiasm or panic of the speculators and non-professionals has been spent. He is not impatient, nor is he even in a very great hurry, for he is an investor, not a gambler or a speculator. The seeds of any bust are inherent in any boom that outstrips the pace of whatever solid factors gave it its impetus in the first place. There are no safeguards that can protect the emotional investor from himself.”

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds.

Fund Notes

As of last week, Strategic Growth Fund remained fully hedged, with a “staggered strike” position that places the strike prices of its index put options moderately below present market levels. The Fund also carries a small contingent call option position representing a small fraction of 1% of assets, as slight insurance against the possibility of a further speculative “blowoff” over the shorter-term. To be clear, we remain defensive overall. Meanwhile, Strategic International remains fully hedged, Strategic Dividend Value is hedged at about 50% of the value of its stock holdings, and Strategic Total Return carries a duration of just over 6 years (meaning that a 100 basis point move in yields would be expected to impact the Fund by about 6% on the basis of bond price fluctuations), with just over 8% of assets in precious metals shares and a small position in utility shares.

Not a peep about this in the liberal MSM. They wouldn’t dare question the murderous policies of dear leader. Malala is a brave girl and tells the thug how terrorism works. American terrorism begets terrorism against America.

The young Peace Prize nominee (who ultimately lost out to the UN-affiliated Organization for the Prohibition of Chemical Weapons), took the opportunity, while the world’s attention was upon her for her brave and fearless efforts, to tell the US president directly that his foreign policy was harming both her home country, Pakistan, and harming US security as well.

Said young Malala in a statement after the meeting:

“I also expressed my concerns that drone attacks are fueling terrorism. Innocent victims are killed in these acts, and they lead to resentment among the Pakistani people.”

She could have played it safe and simply smiled for the camera. Instead she took another huge personal risk for peace. She told the president of the US that he was wrong to make war on her country. Bravo!

Considering past Nobel Peace Prize winners, it is probably better that she did not win. The prize is tarnished.

I’ve noticed numerous MSM mouthpiece articles with the exact same storyline – Obama’s shrinking deficits. They crow about FY13 being the lowest annual deficit of Obama’s presidency. I guess he became fiscally responsible when we weren’t looking. What the stories don’t tell is that the deficit was reduced by over $100 billion from FAKE payments by Fannie Mae and Freddie Mac to the Treasury. There was no money paid, just an accounting entry. These bloated pigs are insolvent, but through accounting gimmicks and failure to mark their mortgages to their true market value, they report billions in paper profits. They then pretend to repay the government. These are sham transactions, but our beloved government leaders know you don’t understand math or Ponzi accounting.

The MSM then must sooth the nerves of their readers by telling them that the deficit as a percentage of GDP is rapidly declining. They fail to mention that our government drones decided to “adjust” GDP up by $500 billion based on a “new” way of looking at things. So, you have a fake deficit number over a fake GDP number to get a much lower percentage. Isn’t that precious?

Earlier this week I saw that fat ass, bloviating, Long Island lawyer pretending to be an investment guru, Barry Ritholtz referencing the deficit at $550 billion and touting this number as proof that Obama and his liberal minions have achieved nirvana. I’m not sure if Ritholtz is really that stupid or just a lying bastard pushing his agenda, along with his books, newsletters, conferences, and worthless investment advice. This is a guy who was stranded for three weeks after Sandy because he was too lazy and dumb to buy a generator.

Maybe fat ass Ritholtz thinks that because the government stopped counting the daily outflow of $2.5 billion per day in May, that meant they weren’t really racking up the debt. If so, he is a bigger tool than I thought. Yesterday we got the truth. After stopping the national debt clock at $16.4 trillion back in May, the drones at Treasury unveiled our new national debt figure:

We sure can spend a lot of money when things are shutdown. The national debt jumped by $329 billion in a single day. Not bad for a days work.

The Treasury has a funky little site where you can run a report on the National Debt by day. Below is the output from September 30 of last year until today.

Let’s do a little math to figure out the true fiscally responsible Obama deficit for FY13.

The government essentially stopped counting on June 1, 2013. The national debt was $16.37 trillion on that day. There were 139 days between then and October 17. The national debt went up by $339 billion over that time frame, or $2.44 billion per day. At that rate, the national debt was really $17.035 on September 30, 2013.

This is where it gets hard for liberals and the math challenged. If the national debt was $16.066 on September 30, 2012 and $17.035 on September 30, 2013, what was the true deficit in FY13?

If you add back the FAKE Fannie & Freddie accounting entries, the true Obama deficit was approximately $1.1 TRILLION. That is only double the number fat ass Ritholtz was quoting.

All hail Obama and his fiscal responsibility.

The cumulative national debt from 1789 until 1982 was $1.1 TRILLION.

| Date | Total Public Debt Outstanding |

| 9/28/2012 | 16,066,241,407,385.80 |

| 10/1/2012 | 16,159,487,013,300.30 |

| 10/2/2012 | 16,171,037,343,408.50 |

| 10/3/2012 | 16,153,318,273,015.00 |

| 10/4/2012 | 16,161,879,857,156.60 |

| 10/5/2012 | 16,161,866,671,342.00 |

| 10/9/2012 | 16,167,932,295,919.50 |

| 10/10/2012 | 16,157,753,419,211.10 |

| 10/11/2012 | 16,158,270,866,947.20 |

| 10/12/2012 | 16,157,542,962,383.10 |

| 10/15/2012 | 16,190,979,268,766.60 |

| 10/16/2012 | 16,199,574,839,671.30 |

| 10/17/2012 | 16,193,100,189,055.20 |

| 10/18/2012 | 16,198,174,452,215.20 |

| 10/19/2012 | 16,196,052,388,163.20 |

| 10/22/2012 | 16,198,677,971,774.40 |

| 10/23/2012 | 16,203,845,445,635.70 |

| 10/24/2012 | 16,194,791,826,674.80 |

| 10/25/2012 | 16,197,082,554,040.00 |

| 10/26/2012 | 16,197,815,714,310.70 |

| 10/29/2012 | 16,198,993,554,072.30 |

| 10/30/2012 | 16,204,061,671,104.80 |

| 10/31/2012 | 16,261,470,510,720.70 |

| 11/1/2012 | 16,221,685,381,838.20 |

| 11/2/2012 | 16,206,129,028,709.20 |

| 11/5/2012 | 16,209,959,246,534.10 |

| 11/6/2012 | 16,214,358,823,745.30 |

| 11/7/2012 | 16,213,982,129,207.30 |

| 11/8/2012 | 16,245,318,820,569.30 |

| 11/9/2012 | 16,244,708,707,467.20 |

| 11/13/2012 | 16,248,293,041,003.50 |

| 11/14/2012 | 16,244,384,093,831.90 |

| 11/15/2012 | 16,278,932,378,520.90 |

| 11/16/2012 | 16,281,329,916,599.60 |

| 11/19/2012 | 16,286,110,428,799.00 |

| 11/20/2012 | 16,292,689,481,349.80 |

| 11/21/2012 | 16,283,161,895,179.80 |

| 11/23/2012 | 16,307,488,943,564.20 |

| 11/26/2012 | 16,309,738,056,362.40 |

| 11/27/2012 | 16,317,681,766,441.40 |

| 11/28/2012 | 16,306,713,138,468.80 |

| 11/29/2012 | 16,323,083,449,604.90 |

| 11/30/2012 | 16,369,548,799,604.90 |

| 12/3/2012 | 16,338,092,943,716.60 |

| 12/4/2012 | 16,347,055,651,380.30 |

| 12/5/2012 | 16,337,928,777,944.10 |

| 12/6/2012 | 16,366,436,891,948.00 |

| 12/7/2012 | 16,365,370,575,377.40 |

| 12/10/2012 | 16,370,056,245,929.60 |

| 12/11/2012 | 16,375,874,429,255.50 |

| 12/12/2012 | 16,366,422,407,639.90 |

| 12/13/2012 | 16,369,984,159,473.80 |

| 12/14/2012 | 16,359,576,959,576.40 |

| 12/17/2012 | 16,351,193,522,286.90 |

| 12/18/2012 | 16,359,758,742,907.70 |

| 12/19/2012 | 16,352,043,784,079.60 |

| 12/20/2012 | 16,334,217,015,073.40 |

| 12/21/2012 | 16,336,217,360,826.40 |

| 12/24/2012 | 16,337,556,561,533.60 |

| 12/26/2012 | 16,337,860,200,635.00 |

| 12/27/2012 | 16,338,243,391,747.00 |

| 12/28/2012 | 16,336,461,552,606.30 |

| 12/31/2012 | 16,432,730,050,569.10 |

| 1/2/2013 | 16,432,705,914,255.40 |

| 1/3/2013 | 16,431,219,143,696.50 |

| 1/4/2013 | 16,432,707,263,449.50 |

| 1/7/2013 | 16,432,671,087,771.60 |

| 1/8/2013 | 16,432,659,028,067.50 |

| 1/9/2013 | 16,432,646,968,419.60 |

| 1/10/2013 | 16,432,692,129,510.80 |

| 1/11/2013 | 16,432,680,097,613.80 |

| 1/14/2013 | 16,432,643,996,680.60 |

| 1/15/2013 | 16,432,632,102,288.60 |

| 1/16/2013 | 16,432,620,067,491.40 |

| 1/17/2013 | 16,432,631,489,854.70 |

| 1/18/2013 | 16,432,619,424,703.00 |

| 1/22/2013 | 16,432,571,159,411.50 |

| 1/23/2013 | 16,432,559,091,945.90 |

| 1/24/2013 | 16,432,567,939,377.30 |

| 1/25/2013 | 16,432,555,923,758.90 |

| 1/28/2013 | 16,432,519,875,802.90 |

| 1/29/2013 | 16,432,507,858,820.40 |

| 1/30/2013 | 16,432,495,841,444.60 |

| 1/31/2013 | 16,433,791,850,294.00 |

| 2/1/2013 | 16,433,779,913,880.30 |

| 2/4/2013 | 16,475,048,398,165.70 |

| 2/5/2013 | 16,480,910,656,603.90 |

| 2/6/2013 | 16,479,954,658,103.50 |

| 2/7/2013 | 16,487,564,297,892.00 |

| 2/8/2013 | 16,488,908,847,828.20 |

| 2/11/2013 | 16,489,930,650,594.10 |

| 2/12/2013 | 16,494,367,339,423.60 |

| 2/13/2013 | 16,524,304,599,079.00 |

| 2/14/2013 | 16,540,800,290,147.40 |

| 2/15/2013 | 16,548,926,805,129.30 |

| 2/19/2013 | 16,552,819,142,207.40 |

| 2/20/2013 | 16,588,751,035,306.30 |

| 2/21/2013 | 16,608,318,357,376.50 |

| 2/22/2013 | 16,609,040,800,845.50 |

| 2/25/2013 | 16,610,557,777,904.90 |

| 2/26/2013 | 16,618,701,810,927.70 |

| 2/27/2013 | 16,607,216,503,950.70 |

| 2/28/2013 | 16,687,289,180,215.30 |

| 3/1/2013 | 16,640,135,316,625.30 |

| 3/4/2013 | 16,649,703,459,968.00 |

| 3/5/2013 | 16,663,709,478,521.00 |

| 3/6/2013 | 16,692,238,790,019.20 |

| 3/7/2013 | 16,701,250,641,109.60 |

| 3/8/2013 | 16,701,846,937,879.70 |

| 3/11/2013 | 16,703,943,129,416.10 |

| 3/12/2013 | 16,709,976,214,794.40 |

| 3/13/2013 | 16,700,634,854,470.50 |

| 3/14/2013 | 16,708,225,460,175.10 |

| 3/15/2013 | 16,731,693,041,858.10 |

| 3/18/2013 | 16,736,188,026,047.80 |

| 3/19/2013 | 16,749,269,587,407.50 |

| 3/20/2013 | 16,739,939,855,865.30 |

| 3/21/2013 | 16,750,130,322,121.00 |

| 3/22/2013 | 16,749,924,938,094.40 |

| 3/25/2013 | 16,753,443,064,898.80 |

| 3/26/2013 | 16,759,063,744,572.40 |

| 3/27/2013 | 16,749,482,454,905.80 |

| 3/28/2013 | 16,766,988,432,792.60 |

| 3/29/2013 | 16,771,379,006,760.30 |

| 4/1/2013 | 16,792,120,009,606.80 |

| 4/2/2013 | 16,804,876,955,116.70 |

| 4/3/2013 | 16,786,970,142,478.80 |

| 4/4/2013 | 16,798,051,589,934.60 |

| 4/5/2013 | 16,797,828,899,086.80 |

| 4/8/2013 | 16,802,515,751,907.60 |

| 4/9/2013 | 16,808,274,414,207.10 |

| 4/10/2013 | 16,798,984,234,792.30 |

| 4/11/2013 | 16,808,067,104,144.00 |

| 4/12/2013 | 16,808,240,386,273.50 |

| 4/15/2013 | 16,801,307,487,216.50 |

| 4/16/2013 | 16,812,065,609,373.20 |

| 4/17/2013 | 16,807,270,364,907.30 |

| 4/18/2013 | 16,779,469,574,292.60 |

| 4/19/2013 | 16,781,967,702,405.30 |

| 4/22/2013 | 16,787,451,118,147.30 |

| 4/23/2013 | 16,798,952,599,955.50 |

| 4/24/2013 | 16,794,349,827,897.30 |

| 4/25/2013 | 16,758,107,082,298.60 |

| 4/26/2013 | 16,756,644,393,707.00 |

| 4/29/2013 | 16,758,168,229,380.20 |

| 4/30/2013 | 16,828,845,497,183.90 |

| 5/1/2013 | 16,805,036,884,755.00 |

| 5/2/2013 | 16,794,979,173,216.60 |

| 5/3/2013 | 16,780,900,194,134.10 |

| 5/6/2013 | 16,788,427,184,539.40 |

| 5/7/2013 | 16,795,552,390,198.40 |

| 5/8/2013 | 16,784,106,881,842.70 |

| 5/9/2013 | 16,754,734,781,812.80 |

| 5/10/2013 | 16,753,992,575,790.10 |

| 5/13/2013 | 16,755,788,437,042.40 |

| 5/14/2013 | 16,760,961,851,934.60 |

| 5/15/2013 | 16,765,040,725,133.70 |

| 5/16/2013 | 16,734,808,644,648.00 |

| 5/17/2013 | 16,737,328,238,148.10 |

| 5/20/2013 | 16,737,294,304,715.50 |

| 5/21/2013 | 16,737,282,992,090.70 |

| 5/22/2013 | 16,734,032,974,210.20 |

| 5/23/2013 | 16,736,576,618,573.30 |

| 5/24/2013 | 16,735,424,271,257.80 |

| 5/28/2013 | 16,737,219,726,401.20 |

| 5/29/2013 | 16,737,208,536,433.80 |

| 5/30/2013 | 16,737,246,099,998.80 |

| 5/31/2013 | 16,738,821,943,986.10 |

| 6/3/2013 | 16,738,788,832,145.30 |

| 6/4/2013 | 16,738,778,336,691.50 |

| 6/5/2013 | 16,738,767,256,596.60 |

| 6/6/2013 | 16,738,770,826,158.50 |

| 6/7/2013 | 16,738,759,828,986.40 |

| 6/10/2013 | 16,738,726,834,732.30 |

| 6/11/2013 | 16,738,715,835,680.50 |

| 6/12/2013 | 16,738,704,836,178.50 |

| 6/13/2013 | 16,738,708,293,971.50 |

| 6/14/2013 | 16,738,697,370,019.80 |

| 6/17/2013 | 16,738,664,595,327.60 |

| 6/18/2013 | 16,738,653,639,711.50 |

| 6/19/2013 | 16,738,642,755,073.30 |

| 6/20/2013 | 16,738,645,811,490.40 |

| 6/21/2013 | 16,738,634,995,209.70 |

| 6/24/2013 | 16,738,602,543,527.10 |

| 6/25/2013 | 16,738,591,725,217.10 |

| 6/26/2013 | 16,738,580,905,836.30 |

| 6/27/2013 | 16,738,629,048,819.00 |

| 6/28/2013 | 16,738,320,054,489.20 |

| 7/1/2013 | 16,738,309,305,648.20 |

| 7/2/2013 | 16,738,298,556,333.20 |

| 7/3/2013 | 16,738,287,806,544.20 |

| 7/5/2013 | 16,738,281,074,058.70 |

| 7/8/2013 | 16,738,249,094,798.80 |

| 7/9/2013 | 16,738,238,434,108.90 |

| 7/10/2013 | 16,738,227,772,946.00 |

| 7/11/2013 | 16,738,230,684,008.80 |

| 7/12/2013 | 16,738,220,086,104.50 |

| 7/15/2013 | 16,738,188,365,630.00 |

| 7/16/2013 | 16,738,177,765,933.40 |

| 7/17/2013 | 16,738,167,165,761.50 |

| 7/18/2013 | 16,738,168,990,385.70 |

| 7/19/2013 | 16,738,158,460,368.60 |

| 7/22/2013 | 16,738,126,867,888.50 |

| 7/23/2013 | 16,738,116,336,111.10 |

| 7/24/2013 | 16,738,105,803,858.20 |

| 7/25/2013 | 16,738,136,405,384.60 |

| 7/26/2013 | 16,738,125,957,131.00 |

| 7/29/2013 | 16,738,094,608,381.00 |

| 7/30/2013 | 16,738,084,158,233.50 |

| 7/31/2013 | 16,738,599,194,294.80 |

| 8/1/2013 | 16,738,600,261,139.00 |

| 8/2/2013 | 16,738,589,818,505.90 |

| 8/5/2013 | 16,738,558,487,748.50 |

| 8/6/2013 | 16,738,548,043,209.60 |

| 8/7/2013 | 16,738,537,598,194.20 |

| 8/8/2013 | 16,738,541,240,281.10 |

| 8/9/2013 | 16,738,530,794,717.40 |

| 8/12/2013 | 16,738,499,455,164.90 |

| 8/13/2013 | 16,738,489,007,693.40 |

| 8/14/2013 | 16,738,478,559,738.10 |

| 8/15/2013 | 16,738,484,642,516.80 |

| 8/16/2013 | 16,738,474,221,654.90 |

| 8/19/2013 | 16,738,442,956,309.10 |

| 8/20/2013 | 16,738,432,533,607.00 |

| 8/21/2013 | 16,738,422,110,434.90 |

| 8/22/2013 | 16,738,460,765,994.00 |

| 8/23/2013 | 16,738,450,395,371.10 |

| 8/26/2013 | 16,738,419,280,739.50 |

| 8/27/2013 | 16,738,408,908,240.10 |

| 8/28/2013 | 16,738,398,535,315.90 |

| 8/29/2013 | 16,738,401,335,152.10 |

| 8/30/2013 | 16,738,649,841,392.70 |

| 9/3/2013 | 16,738,618,787,875.30 |

| 9/4/2013 | 16,738,608,435,751.20 |

| 9/5/2013 | 16,738,608,362,951.80 |

| 9/6/2013 | 16,738,598,129,329.00 |

| 9/9/2013 | 16,738,567,425,782.40 |

| 9/10/2013 | 16,738,557,190,345.30 |

| 9/11/2013 | 16,738,546,954,446.60 |

| 9/12/2013 | 16,738,543,125,208.30 |

| 9/13/2013 | 16,738,533,025,135.60 |

| 9/16/2013 | 16,738,502,722,145.90 |

| 9/17/2013 | 16,738,492,645,235.00 |

| 9/18/2013 | 16,738,482,606,783.00 |

| 9/19/2013 | 16,738,503,812,337.70 |

| 9/20/2013 | 16,738,493,983,660.00 |

| 9/23/2013 | 16,738,464,494,846.80 |

| 9/24/2013 | 16,738,454,664,319.30 |

| 9/25/2013 | 16,738,444,833,205.50 |

| 9/26/2013 | 16,738,443,175,473.90 |

| 9/27/2013 | 16,738,433,470,635.60 |

| 9/30/2013 | 16,738,183,526,697.30 |

| 10/1/2013 | 16,747,478,675,335.10 |

| 10/2/2013 | 16,747,468,940,509.70 |

| 10/3/2013 | 16,747,468,275,799.20 |

| 10/4/2013 | 16,747,458,528,953.00 |

| 10/7/2013 | 16,747,429,285,635.10 |

| 10/8/2013 | 16,747,419,536,935.40 |

| 10/9/2013 | 16,747,409,787,772.30 |

| 10/10/2013 | 16,747,421,858,503.20 |

| 10/11/2013 | 16,747,411,584,091.50 |

| 10/15/2013 | 16,747,370,534,090.60 |

| 10/16/2013 | 16,747,360,549,057.20 |

| 10/17/2013 | 17,075,590,107,963.50 |

It must be those dastardly tea baggers sabotaging the Savior’s glorious, well conceived, well executed, cost saving, life saving healthcare plan for America. Of course a 2,400 page law written by healthcare industry lobbyists, with 11,000 pages of rules and regulations, managed by thousands of government drones, enforced by the IRS, impacting 19% of the U.S. economy, and rolled out on a computer system that doesn’t work, was sure to improve the lives of all Americans. More government in our lives is exactly what we need. Now please bend over and await your Obamacare rectal exam. The $2,500 savings check is in the mail. But be warned, we are depending on another government organization losing $19 billion per year to deliver that check, so it might be awhile.

…Individuals in most states will end up spending more on the exchanges. It is true that in some states, the experience could be the opposite. This is because those states had already over-regulated insurance markets that led to sharply higher premiums through adverse selection, as is the case of New York. Many states, however, double or nearly triple premiums for young adults. Arizona, Arkansas, Georgia, Kansas, and Vermont see some of the largest increases in premiums.

…The Obama Administration is desperate for younger people to enroll to prevent an adverse selection death spiral.

…Our findings confirm that younger populations see larger percentage increases in premiums. A state that exhibits this clearly is Vermont, where the increase for 27-year-olds is 144 percent and the increase for 50-year-olds is still 60 percent, but far less. All states exhibit this relationship.

Heritage Foundation

“If you like your doctor, you will be able to keep your doctor. Period. If you like your health-care plan, you will be able to keep your health-care plan. Period. No one will take it away. No matter what.”

“For people with insurance, the only impact of the health-care law is that their insurance is stronger, better, and more secure than it was before. Full stop. That’s it. They don’t have to worry about anything else.”

“If you already have health insurance, the only thing that will change for you under this plan is the amount of money you will spend on premiums. That will be less.”

“I want to be very clear: I will not sign on to any health plan that adds to our deficits over the next decade.”

“Health care reform will cut the cost of a typical family’s premium by up to $2,500 a year.”

Source:

By: Paul Rosenberg

The Armenian Genocide was a systematic extermination that occurred during World War One, mostly in 1915. The killers were Ottoman Turks: agents and soldiers of that government, as well as eager civilians.

The slaughter took place in two phases. First was the wholesale killing of able-bodied Armenian males through massacre and forced labor. Afterward came the deportation of women, children, the elderly and the infirm, on death marches into the Syrian Desert.

All told, perhaps 1.5 million people were killed. The vast majority of these were Armenians, but the Turks also killed large numbers of Assyrian Christians, Greeks, and other minority groups. In many ways – including that of medical experiments on victims – the Armenian Genocide was the direct forerunner of the Nazi Genocide against the Jews.

Here is one miniscule part of the slaughter – a photo taken by an American diplomat, to which he added a commentary:

“Scenes like this were common all over the Armenian provinces, in the spring and summer months of 1915. Death in its several forms—massacre, starvation, exhaustion—destroyed the larger part of the refugees. The Turkish policy was that of extermination under the guise of deportation.”

The test, believe it or not, is whether people will acknowledge this as a genocide or not.

We live, as I have complained many times, in an age where institutions not only reign over money and lands, but also over men’s minds. And, as it turns out, Armenia is not big enough or threatening enough to matter. And so, the institutional line – world-over and even in some shocking places – has been that “we don’t talk about it.”

The Turkish government, desperate to protect its image, has battled long and hard to explain it all away, and to prevent the word “genocide” from being used. Many, many institutions – tossing aside truth for political expediency – have parroted the Turkish line.

Not everyone has flunked the test. Several European nations have made official statements on the Armenian Genocide, as have a few nations on every continent.

Wikipedia lists 22 nations in all (out of 200).

What I want to focus on here, however, are the two big failures… places that are supposedly dedicated to an ancient philosophy that would instantly and irrevocably condemn the Armenian Genocide as a top-tier evil.

The first failure is the United States.

In an article I wrote earlier this year, I told how my editor (I was then writing for a major publisher) was made to change history textbooks to cut coverage of this story down to just a couple of paragraphs. The US State Department told him to do so because “we need to keep the Turks happy.” My editor’s bosses sided with the government – as people with government contracts nearly always do. Thus the truth, again, became a casualty to institutions.

The one US President to use the word “genocide” was Ronald Reagan, in a speech he made on April 22, 1981. The current US President, Barack Obama, used the word while a candidate for the presidency, but has repetitively refused to use it since. Again, truth dies where institutions reign.

It is of some interest that Reagan, who was a plebeian – not of the elite – was the one exception. Whatever the man’s virtues or vices, he was far less an institution man than presidents of more recent years.

The second flunkee is Israel. That the victims of the signature genocide would fail to recognize the one just before theirs is nothing short of tragic.

Certainly many Israeli and Jewish groups do acknowledge the Armenian Genocide (such as the Union for Reform Judaism), but the Knesset (the Israeli legislature) decided that recognition of this as a genocide would jeopardize relations with the Turks and the Azerbaijanis.

The reason I call this “tragic” is that by refusing to say “genocide,” the ruling Israeli institution turned its back on the great principle that the Hebrews gifted to the world several millennia ago: The enthroning of justice above rulership.

While many individual Israelis are good and decent people, the rulership of the Israeli state has turned away from the original Jewish principle.

As Adolf Hitler was starting his aggression against the Poles, the London Times quoted him as saying this:

Go, kill without mercy. After all, who remembers the Armenians?

For the sake of decency and for the sake of the future, remember the Armenians.

Also remember that justice stands above institutions and rulers.

Paul Rosenberg

[Editor’s Note: Paul Rosenberg is the outside-the-Matrix author of FreemansPerspective.com, a site dedicated to economic freedom, personal independence and privacy. He is also the author of The Great Calendar, a report that breaks down our complex world into an easy-to-understand model. Click here to get your free copy.]

Hat tip to Boston Bob for the video. What exactly are they teaching our kids in high school? And these are the smart kids who made it into college. We are doomed.

This man did whatever he felt was necessary in order to further his agenda; and though it meant making many enemies, he dared look straight into the eyes of both his detractors and those who would defy him, and he never blinked.

He did what had to be done.

But lately he had been trying to find a way out. He didn’t want the responsibility anymore, and he felt as though it was time to quit and leave the empire to whoever was bold enough to seize it.

Sure, he tried to quit, but that wasn’t something he could just do on a whim. Loose ends needed to be tied up, and promises had to be made good and powerful people placated.

For anyone who doesn’t know the outcome of this tale, don’t worry that I might ruin the ending … because that outcome hasn’t been written yet. The best we can do is just guess at how it all plays out.

Wait? What? Oh… Breaking Bad? Nooooo… I wasn’t talking about Walter White, I was talking about Ben Bernanke. Except, he DID blink…

Yes, whilst I was away the Fed announced to the world that, although they had done all the hard work to convince the world that the Dreaded Taper was a done deal that allowed both bond and equity markets to price in a reduction in the amount of asset purchases being made every month by Bernanke (or, as he has become known in financial circles, “Buysenberg”), when it came to crunch time, the Fed didn’t have the guts to pull the trigger. To use the English phrase, “they bottled it”.

Now, any self-respecting drug lord central bank head (hell, any parent) knows that, in order to maintain respect, in order to continue to be feared, you MUST be prepared to follow through with your threats, even if you don’t necessarily want to. That’s just how the world works. You don’t threaten to rain down badness on people and then shy away. If you do that, your credibility is gone and your reputation is in tatters.

In this world, reputation is everything.

In the months leading up to the September FOMC meeting, the world was put on standby for a change in Fed policy, a process that had been innocuously labelled a “taper” by the Fed (check out the video interview with Elliot Management’s Paul Singer in this week’s videos section for an erudite — and I am willing to bet 100% accurate — assessment of how that phrase came to be chosen); and, as the Fed have come to expect in recent years, their preparatory jawboning was working its customary magic.

Source: NY Times

Between May 22, when Bernanke first uttered the T-word, to September 12th, on the eve of the FOMC decision, confidence in the Fed’s beginning their taper climbed relentlessly higher, reaching 67% right before the hammer was supposed to fall.

But a funny thing happened on the way to the forum: the Fed pulled a Cassius Clay and shook up the world….

To continue reading this article from Things That Make You Go Hmmm… – a free weekly newsletter by Grant Williams, a highly respected financial expert and current portfolio and strategy advisor at Vulpes Investment Management in Singapore – please click here.

These slimy weasels are bought and sold like cheap whores. Sorry for the insult to all my cheap whore readers. Mitch McConnell is everything that is wrong with this country rolled into one disgusting package of shit. Kicking the can and bending over for Harry Reid and the Obamanistas are his specialty. When he was the Senate Leader the Republicans cut nothing. He added trillions to the national debt when he was in control. We are a deadbeat nation led by corrupt brain dead old men. This turtle faced douchebag needs to be crushed by a truck while crossing the road.

A proposal to end the government shutdown and avoid default orchestrated by Republican Leader Mitch McConnell and Democratic Leader Harry Reid includes a nearly $3 billion earmark for a Kentucky project.

Language in a draft of the McConnell-Reid deal (see page 13, section 123) provided to WFPL News shows a provision that increases funding for the massive Olmsted Dam Lock in Paducah, Ky., from $775 million to nearly $2.9 billion.

The dam is considered an important project for the state and region in regards to water traffic along the Ohio River.

As The Courier-Journal’s James Bruggers reported in 2011, the U.S. Army Corps of Engineers said they needed about $2.1 billion for the locks due to “stop and go funding.”

Asked about the additional funding in the proposal, McConnell spokesman Robert Steurer directed all questions to lawmakers who worked on the bill directly.

“Senators (Diane) Feinstein and (Lamar) Alexander, the chair and ranking member of the energy and water subcommittee, worked on the issue and can help you,” he says.

Since 2009, McConnell has been an outspoken supporter of the project, and has been working on getting its funding for some time.

Watch:

Still, conservative critics of the proposal argue it is nothing more than a “kickback” for McConnell in an age where Tea Parties have eschewed earmarks.

The Olmsted Dam sees nearly 90 billion tons of materials such as coal, petroleum and other goods move through that stretch of the Ohio River annually.

UPDATE 7:30 p.m.:

A statement from Sen. Alexander’s office to BuzzFeed says the language was added to prevent funding from being canceled.

“According to the Army Corps of Engineers, 160 million taxpayer dollars will be wasted because of canceled contracts if this language is not included. Sen. [Diane] Feinstein and I, as chairman and ranking member of the Energy and Water Appropriations Subcommittee, requested this provision. It has already been approved this year by the House and Senate.”

UPDATE 9:35 p.m.:

The Senate passed the McConnell-Reid deal by a 81-18 vote and it now heads to the House.

Among those who voted against the bill were Sen. Rand Paul of Kentucky, who derided the legislation for overlooking the nation’s debt.

“Tonight, a deal was struck to re-open the government and avoid the debt ceiling deadline. That is a good thing,” Paul said in a statement. “However, our country faces a problem bigger than any deadline: a $17 trillion debt. I am disappointed that Democrats would not compromise to avoid the looming debt debacle.”

Paul’s office has not responded to our request for commenting regarding the provision for the Olmsted project.

In a follow-up e-mail, McConnell’s office told the radio station the GOP leader did not request Alexander put wording to raise the authorization for funding in the bill despite McConnell’s support for earmark funding in the past.

It won’t be the free shit army leading the revolution. They are still getting their free shit and are satisfied living a life of ignorance and squalor. It is the educated middle class who have fallen into the lower class that are most angry. They believed in the American dream and it has proven to be an illusion. Their anger is palatable as they witness the continued looting by the Wall Street elite and the transfer of their wealth to the non-productive ignorant class through SNAP, SSDI, Section 8 housing and a myriad of other entitlement bribe programs.

The spark for any revolution would have to come from the youth of the country who have been enslaved in the chains of $1.2 trillion of student loan debt, no job prospects, and being handed a $200 trillion bill by their parents and grandparents. When will their frustration and anger boil over? There will be a revolution and I want to be there when Jamie Dimon, Bernanke and the other criminals lose their heads. Bring it on.

By Paul B. Farrell, MarketWatch

SAN LUIS OBISPO, Calif. (MarketWatch)

Credit Suisse’s new Global Wealth Report reminds us of the 1790s when inequality ignited the French Revolution and 40,000 met the guillotine. Today, Credit Suisse data reveal that just 1% own 46% of the world, while two-thirds of the world’s people have less than $10,000 wealth.

Credit Suisse predicts a world with 11 trillionaires in a couple generations, as the rich get richer and the gap widens.

Can this trend continue? Or will it trigger an “economic guillotine?” Nobel economist Joseph Stiglitz, author of “The Price of Inequality,” is not as optimistic as Credit Suisse: “America likes to think of itself as a land of opportunity.” But today the “numbers show that the American dream is a myth … the gap’s widening … the clear trend is one of concentration of income and wealth at the top, the hollowing out of the middle, and increasing poverty at the bottom.”

History is warning us: Inequality is a recipe for disaster, rebellions, revolutions and wars. Not in two generations. Much, much sooner, a reminder of the Pentagon’s famous 2003 prediction: “As the planet’s carrying capacity shrinks, an ancient pattern of desperate, all-out wars over food, water, and energy supplies will emerge … warfare will define human life on the planet by 2020.” Yes, much sooner than two generations.

Revolutions catch us off-guard, ignite suddenly, spreading like fire The French Revolution is a powerful history lesson, easily denied. Angry masses. Their treasury bankrupt. High interest on nation debt consumed half their tax revenues. Why? Earlier wars, a decedent aristocracy, an incompetent King Louis XVI. The anger so intense that during the 1792-93 Reign of Terror the king was guillotined, along with as many as 40,000 others, many of whom were innocent, as inequality ripped apart their nation.

Why? The aristocracy, intellectuals and the rich were oblivious of the needs of the masses, much like our leaders today. As Adbusters magazine put it: “Even in the seconds before their heads were about to roll away from their bodies underneath the blade of the guillotine, it still puzzled the opulent Paris elite how this could be happening.”

The truth is, they were in denial, not listening to the masses for years. Yes, revolutions catch whole nations by surprise: “Just months before the storming of the Bastille in 1789, everything was peachy. The social order ran smooth. The poor paid their dues. The middle class kept their mouths shut. The aristocracy partied … and the next day they were being dragged through the streets by their frilly collars like common thieves.”

Inequality is accelerating rapidly to revolutionary levels Are we near a new Bastille Day today? Barry Ritholtz’s the Big Picture recently posted “The Stunning Truth About Inequality In America,” a list of 14 reasons from “WashingtonsBlog,” warning us the inequality gap is accelerating rapidly, widening so fast that America may soon be at what you could call Bastille Day levels, an inequality gap so great it is the fuel and trigger that can ignite an angry people into revolution.

These 14 triggers are reinforced by the statistics in the Credit Suisse Wealth Report, Stiglitz’s challenge and the Pentagon prediction. Here’s a slightly edited version of the “Stunning Truth About Inequality,” a must-read for America’s 95 million of investors:

1. It’s worse than you imagine. Americans consistently underestimate the amount of inequality in our country. They would be shocked to learn the truth …

2. Worse than history’s worst. Twice as bad as in ancient Rome, worse than in tsarist Russia, worse than in America’s Gilded Age, worse than in modern Egypt, Tunisia or Yemen, worse than in many banana republics in Latin America. Yes, today’s inequality is even worse than experienced by slaves in 1774 colonial America.

3. America lagging other developed nations. Worse in America than any other developed nation.

4. Permanent inequality. Staggering inequality in America has become permanent.

5. America’s two economies. There are two economies: one for the rich, and the other for everyone else.

6. Top 1% rallys, while 99% in recession. The economy has only recovered for the richest 1% … the rest of the country is more or less stuck in a depression.

7. Rich keep getting richer. The Super Rich are raking in more than ever before.

8. Poor getting poorer. While more and more people are sliding into poverty.

9. Middle class now dead. One of every five households in the America is on food stamps. The middle class has more or less been destroyed.

10. Causes market crashes. Who’s who of prominent economists and investors say that inequality causes crashes and hurts the economy.

11. Great Depression. Extreme inequality helped cause the Great Depression, the current financial crisis … and the fall of the Roman Empire.

12. Bad political policies. Inequality isn’t happening for mysterious or uncontrollable reasons. Bad government policy is responsible for runaway inequality.

13. And leadership. Bush was horrible, but income inequality has increased even more under Obama than under Bush.

14. Conservatives. It’s a myth that conservatives accept runaway inequality. Conservatives are as concerned as liberals regarding the stunning collapse of upward mobility.

Even if the Super Rich do avoid the coming economic guillotine, what’s ahead? In “Wealth, War and Wisdom,” hedge fund manager Barton Biggs, former Morgan Stanley global strategist, warned of the “possibility of a breakdown of the civilized infrastructure,” a revolution of the disillusioned, angry masses. His solution? Buy a farm up in the mountains: “Your safe haven must be self-sufficient and capable of growing some kind of food … well-stocked with seed, fertilizer, canned food, wine, medicine, clothes, etc. Think Swiss Family Robinson.”

Hat tip to BostonBob for sending this to me.

“Think of how stupid the average person is, and realize half of them are stupider than that.” – George Carlin

Hat tip to Hope.

Only 5% of the population in my county is on SNAP. But the number has gone up by 230% since 2000. The population of my county is up about 3% since 2000.

In the urban kill zone of Philadelphia, the total is 27%. They don’t break it out by sections of the city, but I would bet that the 30 Blocks of Squalor exceeds 50%.

I wonder what the 450,000 Phila SNAP recipients will do when their pretty little SNAP cards stop working?

The unsustainable cannot be sustained.

Since the turn of the millennium, participation in the food stamp program, known officially as the Supplemental Nutrition Assistance Program, has more than doubled to 15 percent of all U.S. residents in January. In some parts of the country, as few as 1 in 20 people receive food stamps. In others, the figure is more than 1 in 3. Low-income households that meet SNAP eligibility requirements receive a payment card that can only be used to buy government-approved essential foods.

Under President Obama’s watch, the value of the benefits distributed by the program each year has more than doubled as more people have fallen below the poverty line and more households have joined the program. Obama has expanded eligibility under the theory that it helps the economy, which led Newt Gingrich to dub him the “food stamp president” early in the 2012 election season. Due to the high unemployment rate, the Obama administration has also waived a 1996 job requirement—a rule that made finding a job or enrolling in job training a prerequisite for receiving SNAP benefits—for 46 states. Republican leaders are trying to reinstate the requirement to counteract the program’s escalating cost.

To find out how many people participate in the program in your area and how that number has changed since 2000, enter your ZIP code, city, or county and state in the link below.

“Mr. Speaker, I once again find myself compelled to vote against the annual budget resolution for a very simple reason: it makes government bigger.”

― Ron Paul

“When the federal government spends more each year than it collects in tax revenues, it has three choices: It can raise taxes, print money, or borrow money. While these actions may benefit politicians, all three options are bad for average Americans.”

― Ron Paul

“One thing is clear: The Founding Fathers never intended a nation where citizens would pay nearly half of everything they earn to the government.”

― Ron Paul

“We need to understand the more government spends, the more freedom is lost…Instead of simply debating spending levels, we ought to be debating whether the departments, agencies, and programs funded by the budget should exist at all.”

― Ron Paul

“Failure of government programs prompts more determined effort, while the loss of liberty is ignored or rationalized away…whether is it is the war on poverty, drugs, terrorism…or the current Hitler of the day, an appeal to patriotism is used to convince the people that a little sacrifice of liberty, here or there, is a small price to pay…The results, though, are frightening and will soon become even more so.”

― Ron Paul

“The most basic principle to being a free American is the notion that we as individuals are responsible for our own lives and decisions. We do not have the right to rob our neighbors to make up for our mistakes, neither does our neighbor have any right to tell us how to live, so long as we aren’t infringing on their rights. Freedom to make bad decisions is inherent in the freedom to make good ones. If we are only free to make good decisions, we are not really free.”

― Ron Paul

“A system of capitalism presumes sound money, not fiat money manipulated by a central bank. Capitalism cherishes voluntary contracts and interest rates that are determined by savings, not credit creation by a central bank.”

― Ron Paul

“Let it not be said that no one cared, that no one objected once it’s realized that our liberties and wealth are in jeopardy.”

― Ron Paul