Guest post from John Wilder – you can subscribe to him here

“Why don’t we pretend he didn’t die? Just for a bit . . .” – Weekend at Bernie’s

Why can’t Ray Charles drive? He’s dead. (Outside of this one, memes are “as found”)

On March 15, 44 B.C., Julius Caesar was walking to work, since Rome was declared by Gretanius Thunbergium to be a “walkable city” because she was concerned about the sweat of galley slaves and horses making the oceans too salty, thus enraging Neptune, the god of the sea.

This particular day was a good one in Rome, and the bright warm Sun shone down on Caesar as he made it to the Senate. Caesar loved the Senate, since all of the Senators were really cool and he loved hanging out with them to watch the gladiator games every Sunday.

Then, on arriving at the Senate? Caesar was stabbed in the back by raising interest rates, and, with his last, dying words, he said, “Please, take this salad dressing, and remember me by it. Oh, and name a way that babies are born after me. And Kaiser and Czar might be cool titles for kings in the future.”

Okay, that might not be exactly what happened. But you can’t prove it wasn’t, because it’s not on YouTube®.

But interest rates have been a thing since long before even Julius Caesar crossed the Rubicon, took the throne, and then became a human pincushion. And they’ve been gumming up society both before then, and also since then.

Last Friday, on March 10, a curious thing happened – the 19th largest bank, Silicon Valley Bank, went tango uniform. To paraphrase Python, Monty:

“It’s a stiff. Bereft of life. It rests in peace. If you hadn’t backfilled the coffers with Federal Reserve® notes, it would be pushing up daisies. Its metabolic processes are now history. It’s off the twig. It’s kicked the bucket. It’s shuffled off the mortal coil, run down the curtain and joined the bleeding choir invisible. THIS IS AN EX-BANK.”

How, exactly, does a Norwegian blue parrot bank die so quickly?

The truth is, it has been dead for a bit. I’ll explain. You can get explanations of this elsewhere, but none of them will be as funny, since that’s what my job is.

When banks take in money, they have several options of what they can do with it. They can bury it in Mason® jars in the back 40, they can loan it to other people, or they can park it in an investment. Back in 2008, the big financial crisis was that the loans were to people that could never have paid the money back. I was offered a guaranteed approval home loan on a house (with zero down!) that was ten times my income.

“Why would you offer me that? I could never pay that back?” was my response.

The loan lady sighed audibly over the phone. “I know, but I’m required to tell you that.”

It’s like they never learned anything.

So, part of the problem in 2008 was that the loans were junk because some folks said, “I could use a pool surrounded by marble columns with a champagne fountain built out of PEZ™. I’m in!” even though they only made $32 dollars a month. They even had a name for these loans – NINJA – “No Income, No Job”.

These banks also gambled with the cash of the average depositor, investing in champagne PEZ© fountain manufacturers. Hey, how could they lose?

Oh, yeah. Things don’t go up forever. So when they end? It gets ugly.

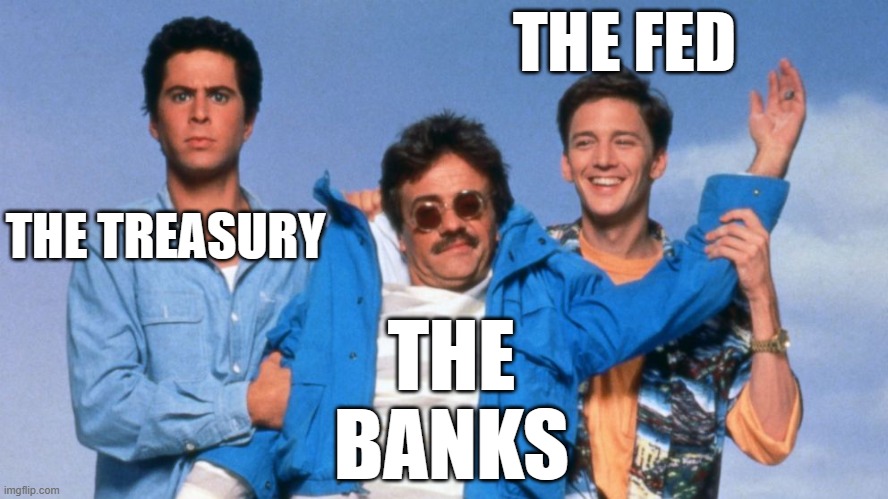

The response to that by the Fed® was to use a cash cannon and barrage the banks. The idea was this, the banks would soak up the cash to paper over the bad debts, and if they had extra cash, they’d park it at the Fed™. Essentially, the Fed™, working with the banks, made sure that the bankers could keep getting big bonuses, not face criminal charges like the average small-town banker might if he stole the cash from the deposits to pay for his 4.5 out of 10 mistress and trips to Vegas.

It’s like there are different rules for you and I.

Nope. They got to keep their penthouses, private jets, and bimbos. In order to keep this nonsense so it wouldn’t implode, the one thing the Fed™ had to do was keep interest rates low. If the Fed© had tried this in 1975, or 1985, or 1995, the world would have punished it by driving the value of the dollar down (faster), cratering purchasing power and the economy.

But after 2008, there was no other big power. Japan was a basketcase, Europe was still the Jekyll an Hyde level continent, with Western Europe mainly concerned about how many “Syrians” they could import, and Eastern Europe mainly working out how to make more potatoes so they could make more vodka. Roads? Why?

That left the United States as, amazingly, still the only kid with a currency anyone trusted, even though we were spending like a sixteen-year-old with dad’s credit card.

Huh, wonder when YouTube® will ban people for this?

Oh, the Left is already trying to censor people. Nevermind.

I like the cut of his jib.

Not now. The COVID world created the Trump/Biden policy of “How can we spend more money today?” Contrast that with China’s “No body count is too high” policy, and, oddly, the world began to trust the United States less. Add in Biden’s incoherent policy of a.) letting wars start and b.) pushing away allies like the Saudis, and now we live in a world driven by chaos.

And we’ve lost the trust of the world.

So, the banks still do the same three things with the cash deposited in their banks: Mason™ jars in the backyard, loan it, or invest it. Last time, the banks invested in whatever crap floated in the window. That was silly.

The banks thought they had cracked the code: this time, they invested in U.S. Treasury Bonds.

Yay! That’s what a sober person would do, right?

Well, maybe. But when a bank buys a 10-year bond that has an attached interest rate of 0.08%, and the stated inflation rate is 6%, the value of that 10-year bond craters. Interest rates go up? Bond values go down. It turns out Silicon Valley Bank™ had some of these bonds. How many? Enough to wipe out all of the shareholder and bondholder (yeah, they bought and sold bonds) value. And it’s not limited to them. Here’s the take on the unrealized losses of the biggest banks in America:

Losers in 1901, Losers in 1921, Losers in 1929, Losers in 1937, Losers in 1945, Losers in 1948, Losers in 1953, Losers in 1957, Losers in 1950, Losers in 1960, Losers in 1969, Losers in 1973, Losers in 1980, Losers in 1981, Losers in 1990, Losers in 2001, Losers in 2007 . . . Oh, wait, the banks didn’t lose anything, it was just regular people.

The FDIC insures deposits to $250,000. Except when (reportedly) Oprah had half a billion in that particular bank. Turns out that the United States blinked: “You get all your money, and you get all your money, and you get all your money,” because Oprah is more important than you and I.

Two other banks have failed already. You can see that some of their CEOs were serious people only worried about the welfare of their depositors.

Yup, the “adults” are in charge.

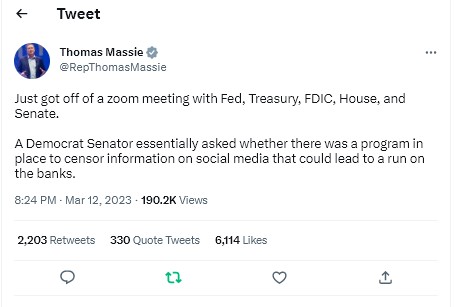

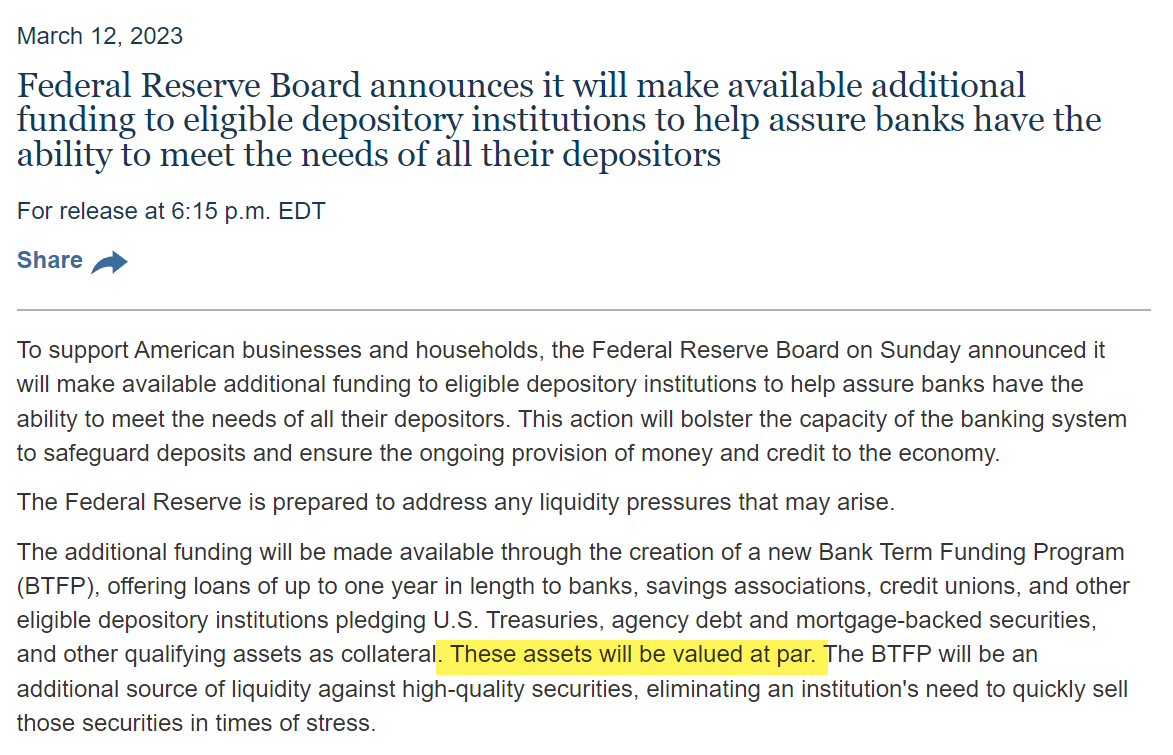

This will not result in an immediate run. The Fed® and the Treasury will continue to backstop the banks because to do otherwise would collapse the system. They even say so. Valuing assets “at par” means at what the banks paid for them. I own a car from 2003. In Fedspeak® that asset would be valued at the initial purchase price, despite the fact that it has one light-second worth of miles (kilopascals) on it. Here’s proof:

See? I’m a respected journalist. Besides, I believe I am the VERY FIRST person to note that the reserve ratio had gone to zero. You can check it out. This will help my lawyer if I’m ever sued. (Serious about the very first part.)

The Fed™ is screwed. They want to keep Biden in office, which requires low interest rates and a booming economy and no inflation. But to lower inflation, they have to jack up the interest rates far above the rate of inflation. Biden cannot be re-elected. Period, unless there’s a global war.

Nah, people would never buy a war started due to economic issues.

Ooops. I’d say sorry, but this is already in the playbook.

Me? My bet is this can keeps rattling around causing damage for several months. Six or seven? Maybe. Eventually, the Fed® is going to figure out that they can’t paper over this mess.

In the meantime, the cash for businesses will dry up, and the only people that can borrow money will be those that don’t need it. New projects? They’ll be cancelled unless the company has the cash or it will ruin them if they don’t stop. New housing? Forget it. The housing market will collapse, (it already is) and the costs of new stuff to make new are so high that no one can afford it, forget the interest rate.

People will stop eating dinner in a restaurant. We already have.

No, the Ides of March won’t be the end. But you can see it from here. While you can, enjoy the nice walk on a sunny day.

And Neptune? He’s always been a whiney bitch. Ignore Neptune.

Thomas Massie has more street smarts and horse sense than Trump , and is a FAR better judge of character.

The only person in Congress who’s figured out that Oliver Wendell Holmes’ famous formulation is full of every kind of horseshit.

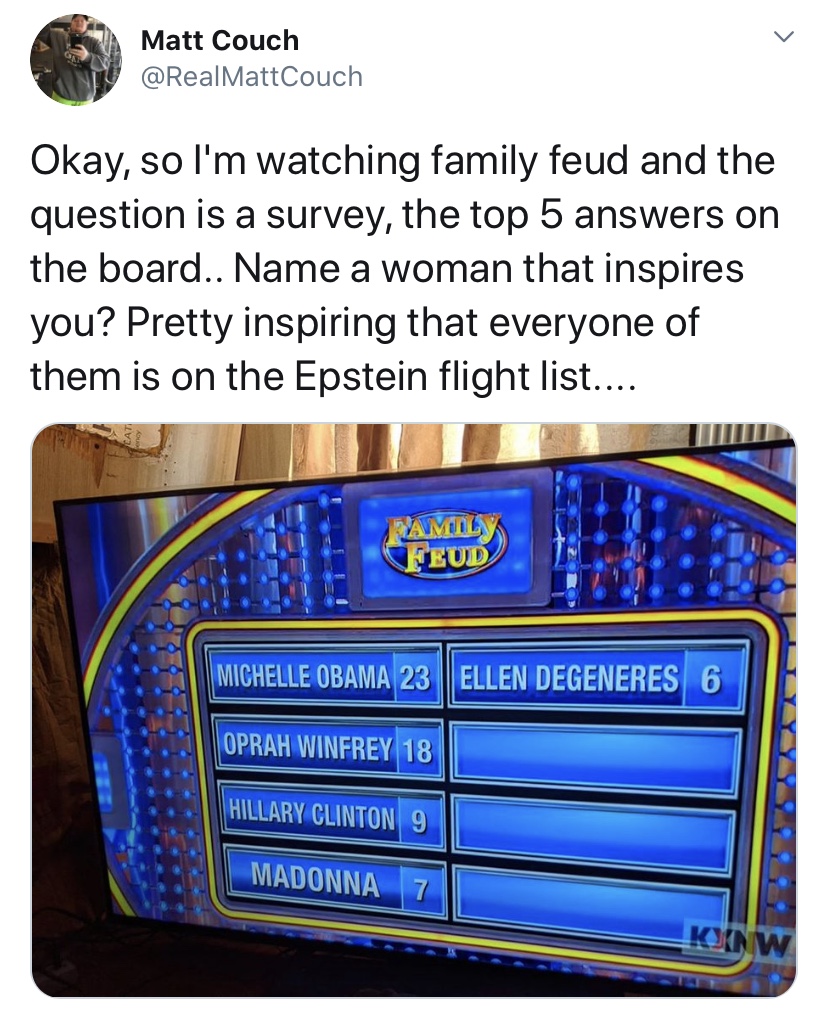

WRT that Family Feud survey –

Michelle Obama is a man.

C’mon people, deep down you know you want this stinking shit pile we call Neo-liberal Democracy to collapse.

Deep down?

I wear it on my sleeve.

My preferred method

Seems to work pretty good.

I gotta go get some range time today… going going…

john,

your usual good column but we need BIKINIS —

note the need,not the want —

Dominion, the dead and mail in voting will decide that thank you very much.

John is always interesting. Bought the Bank Run t-shirt weeks ago. Wore it into town last week. Lotsa laughs. And a few scowls.

Who else expects total anarchy in the urban centers this summer?

Fleischmann, Bankman-Fried, and Neumann. Huh.

imagine that….

When do the gloves come off? When they do, don’t let them EVER get back up:

Various bits in the article speak about Biden’s “election”, eg, “You get what you vote for…” and “Biden will be unelectable…” etc etc.

News Flash – no-one “voted” for Biden, and he was NEVER “elected”, nor will he be “elected” in future.

You get what your masters give you.

And you all bend over and say “Thank you sir, may I have another?”.